Nadex Co

Smart capital allocation, under 1/2 of TBV.

This new Japanese net-net that I found fits many of the criteria I look for:

Discount to NCAV

Decent earnings yield

Stable business

Smart capital allocation

Pays dividends and compounds tangible book value per share

The only aspect that Nadex (TYO 7435) lacks compared to other Japanese stocks is its cash-to-market cap ratio, which is a meager 47%. In the US, this is unheard of, but in Japan, it is considered a very aggressive capital return policy.

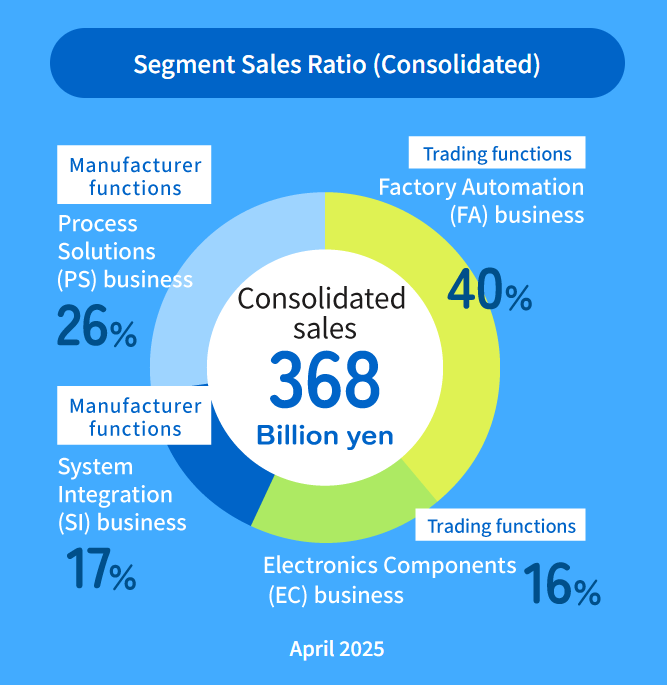

Nadex is a small Japanese trading company with a few reportable segments:

In the last 10 years, Nadex has very slowly grown revenues while not reporting a single operating or net loss:

Nadex has generated ¥8.27 billion in net income in the last 9 fiscal years on ¥132.9 billion in net tangible assets, for a 6.2% return on net tangible assets. While nothing extraordinary, the company is generating acceptable returns on its capital.

Valuation

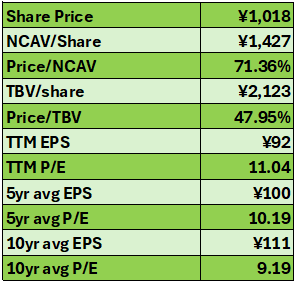

Paying 1x TBV for a company that generates 6% on that is not a great deal. But Nadex is trading under ½ of TBV. This implies you’ll get about a 13% return at current prices if the company can keep generating the same returns.

The valuation is pretty simple here: it’s trading for 71% of NCAV, 48% of TBV, and 10x normalized earnings.

Balance Sheet

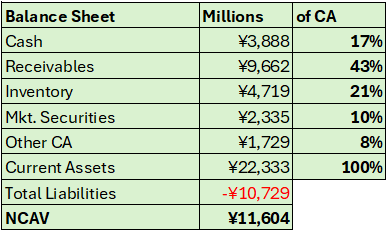

Nadex’s balance sheet is pretty solid; 70% of the current assets are comprised of cash, receivables, and marketable securities. This reduces the chances of your assets being impaired compared to a company that holds 90% in inventory. The ratio of current assets to total liabilities is over 2, which is a small sanity check I like to do.

Note: the marketable securities line is likely understated because Nadex doesn’t break down its investment line within quarters, so I’m using the FY 2025 figure. Its total “investments” line grew 25% since.

Capital Allocation

Nadex is one of those Japanese companies that understands capital allocation. They have been buying back shares consistently since FY 2023. Reducing total sharecount by 12.7% since and 3.2% in the last 12 months. They are conducting these repurchases under NCAV and under ½ of TBV, which implies their repurchases are yielding >12%. This should allow the stock to close the gap between the current price and NCAV.

One aspect I like looking at is the ability of the company to raise dividends in the future. Nadex is paying out about ⅓ of its earnings in dividends each year. If they continue to repurchase 3-4% of shares each year, they should be able to raise dividends at that rate without increasing the payout ratio. On top of that, there is room to increase the payout ratio to, say, 50%, which should drive the stock price up.

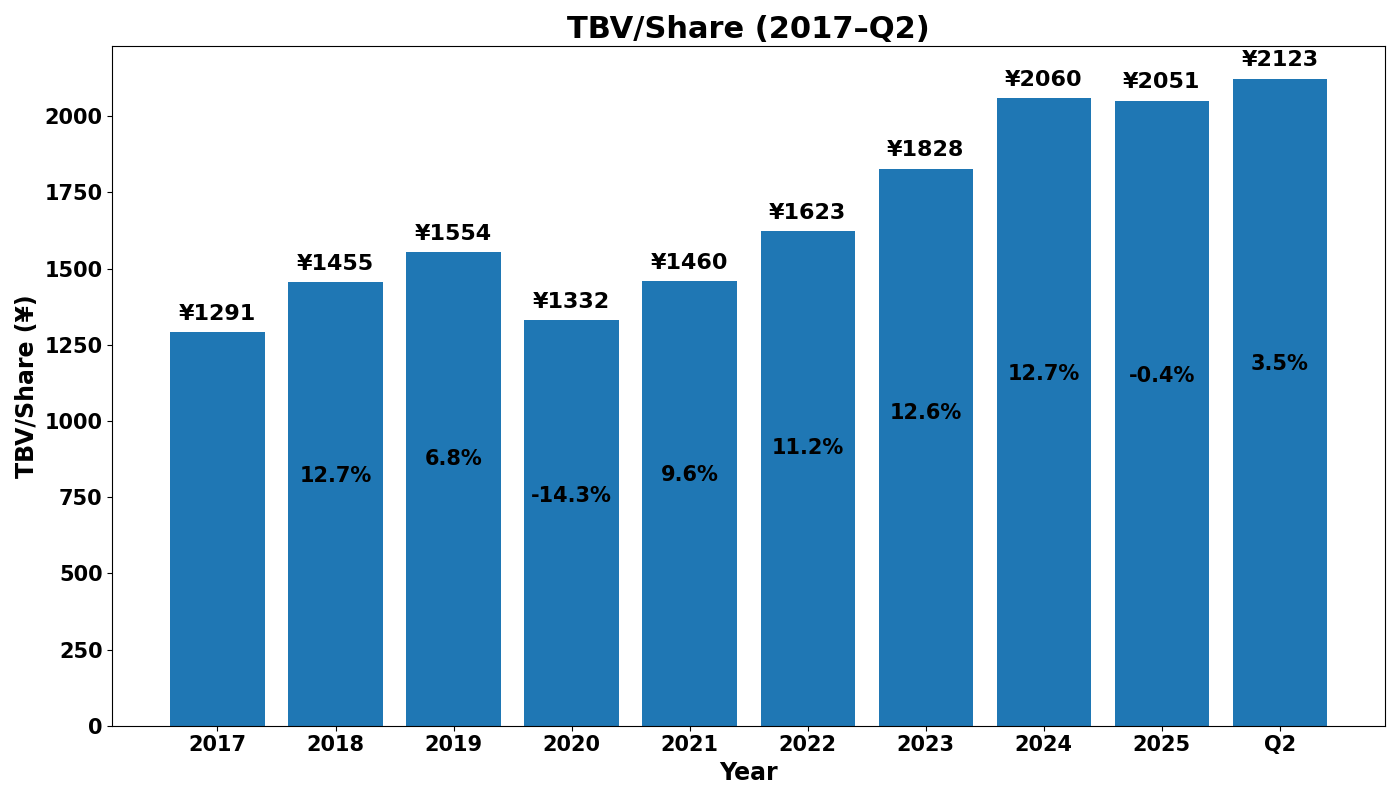

I always keep in mind that when I buy a net-net, any optionality to increase shareholder returns is welcome. I think my best returns come mostly from selling when stock prices pop to NCAV after an announcement to raise dividends. It’s also nice that the company has compounded TBV per share at 6.4% for the last 10 years and 7.7% in the last 5. This means that the company is becoming more valuable as I wait for something to happen.

How might this investment go wrong?

In these write-ups, I always answer this question in a similar fashion. I usually do not know a lot about the underlying economics of the business or why the business exists. There’s the risk of shareholder returns stopping, creating a value trap. And sometimes some other factor that is individual to the specific company. The truth is that most businesses I acquire have similar risks. But when I started buying Japanese net-nets, I was extremely careful and conservative, and I asked my brother: After buying a basket of companies with these characteristics, what’s the likelihood that we lose money in 3 years? I think giving a straight answer may be hubris; I think the answer is “low.”

Long Nadex TYO: 7435